Sunday, August 10, 2008

Tuesday, July 1, 2008

So Now What?

All right, I've given you pretty much a brain dump of what I think of the oil situation. I didn't want to leave things in such a negative state, and I wanted to share what my personal thoughts are as far as going forward is concerned.

It goes something like this.

As long as our cars run on gasoline:

The obstacles are technical at this point. Importantly, they are not infrastructural. Unlike hydrogen or other new physical commodities as fuels, no new pipelines or fueling stations or rails or other major infrastructure projects are creating a chicken or the egg type situation. (For instance, in order to use hydrogen powered cars, you need hydrogen fueling stations - which no one will build until there are hydrogen cars - which no one will buy until there are hydrogen fueling stations.)

The main technical obstacle is battery technology. Fortunately, there is a great deal of work going on in batteries and progress is being made. Also, all the car manufacturers are moving towards hybrids of one type or another. So, things are in the works.

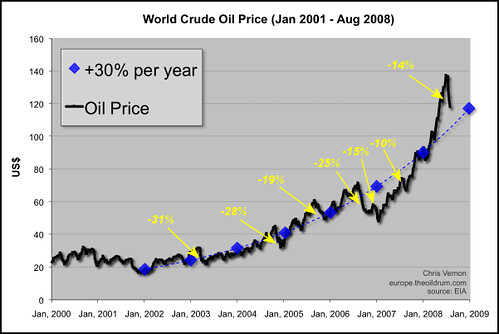

But this is all on a timer. According to the oildrum.com (which seems like a pretty good source), peak oil was in 2005 with a shallow decline happening until 2011, at which point the decline accelerates.

There is going to be a race between reducing our reliance on oil and the falling rate of oil production. Things are already in motion, and some rational decisions are begin made.

First, people are actually driving fewer miles at this point. The number of miles driven in the United States has now fallen (for the first time in at least 20 years) for the past 2 years. Also, automotive manufacturers are closing minivan and truck plants, and changing their product mix to smaller vehicles due to changing market demands. A number of plug-in hybrids (which are both electric and gasoline powered) are coming between 2009 and 2011. This will reduce demand and make the oil last longer.

Second, I think we should drill domestic continental shelf oil and even ANWAR. We should also clear up the legal obstacles preventing land that should be drill-able from actually going into production. This will slow the reduction in production (specifically 5-7 years from now when we will really need to slow the decline).

Third, I believe we should begin building new electric power plants (pick your flavor - nuclear and coal seem the best at this point). This should be done because parts of the country are already near electric capacity, and if we bring our transportation system to electric, we are going to need more power. Fortunately, coal is cheap, and nuclear isn't anymore expensive than it always has been. This gets us ready for an electric future.

And, fourth, we should let the market work. Solar costs are going to come down, and lots of other really neat stuff will be developed to meet demand. We've done something like this once before in the 1970s. Much more of our industry was based on oil, but since then, really just our transportation is totally reliant.

To sum up, the race is on. Get transportation off of oil, before it puts the brakes (and even reverse thrusters) on the global economy.

It goes something like this.

As long as our cars run on gasoline:

- the number of nuclear power plants are irrelevant to transportation prices.

- the number of coal plants are irrelevant

- the number of natural gas plants are irrelevant

- the number of solar plants are irrelevant

- the number of wind plants are irrelevant

- the number of thermal plants are irrelevant

- the number of hydroelectric plants are irrelevant

- etc., etc., etc.

The obstacles are technical at this point. Importantly, they are not infrastructural. Unlike hydrogen or other new physical commodities as fuels, no new pipelines or fueling stations or rails or other major infrastructure projects are creating a chicken or the egg type situation. (For instance, in order to use hydrogen powered cars, you need hydrogen fueling stations - which no one will build until there are hydrogen cars - which no one will buy until there are hydrogen fueling stations.)

The main technical obstacle is battery technology. Fortunately, there is a great deal of work going on in batteries and progress is being made. Also, all the car manufacturers are moving towards hybrids of one type or another. So, things are in the works.

But this is all on a timer. According to the oildrum.com (which seems like a pretty good source), peak oil was in 2005 with a shallow decline happening until 2011, at which point the decline accelerates.

There is going to be a race between reducing our reliance on oil and the falling rate of oil production. Things are already in motion, and some rational decisions are begin made.

First, people are actually driving fewer miles at this point. The number of miles driven in the United States has now fallen (for the first time in at least 20 years) for the past 2 years. Also, automotive manufacturers are closing minivan and truck plants, and changing their product mix to smaller vehicles due to changing market demands. A number of plug-in hybrids (which are both electric and gasoline powered) are coming between 2009 and 2011. This will reduce demand and make the oil last longer.

Second, I think we should drill domestic continental shelf oil and even ANWAR. We should also clear up the legal obstacles preventing land that should be drill-able from actually going into production. This will slow the reduction in production (specifically 5-7 years from now when we will really need to slow the decline).

Third, I believe we should begin building new electric power plants (pick your flavor - nuclear and coal seem the best at this point). This should be done because parts of the country are already near electric capacity, and if we bring our transportation system to electric, we are going to need more power. Fortunately, coal is cheap, and nuclear isn't anymore expensive than it always has been. This gets us ready for an electric future.

And, fourth, we should let the market work. Solar costs are going to come down, and lots of other really neat stuff will be developed to meet demand. We've done something like this once before in the 1970s. Much more of our industry was based on oil, but since then, really just our transportation is totally reliant.

To sum up, the race is on. Get transportation off of oil, before it puts the brakes (and even reverse thrusters) on the global economy.

Monday, June 30, 2008

Speculators Doing Their Thing

I saw this today at Bloomberg. The article is about how high commodities prices led to increased plantings of corn and wheat. How convenient for me that they demonstrate my point in such a timely fashion.

From the article:

"June 30 (Bloomberg) -- Corn fell the maximum permitted by the Chicago Board of Trade and wheat dropped the most in 13 weeks after the government said U.S. farmers planted more of both crops than previously expected."

From the article:

"June 30 (Bloomberg) -- Corn fell the maximum permitted by the Chicago Board of Trade and wheat dropped the most in 13 weeks after the government said U.S. farmers planted more of both crops than previously expected."

Sunday, June 22, 2008

OPEC Mumbo Jumbo

Lately, the leaders of OPEC say the high price of oil is due to speculators, and taxes, and even irrationality. Everything except the fact that they cannot meet global demand.

My view is that it is in their interest to maintain the status quo in terms of the demand structure of the global economy as long as possible. And, by demand structure, I mean the heavy reliance on their product for transportation.

Suppose for a moment that the shortage of oil is permanent and real. As soon as most people come around to this realization, the global transportation system will begin to transition away from oil. That transition will end the oil state as it exists today.

Many OPEC members are currently engaged in huge infrastructure projects and are attempting to diversify their economies. The longer they have to develop these projects, the better chance they have of not becoming impoverished when the oil demand dries up.

So, don't expect to hear anything from them about limited supply any time soon.

My view is that it is in their interest to maintain the status quo in terms of the demand structure of the global economy as long as possible. And, by demand structure, I mean the heavy reliance on their product for transportation.

Suppose for a moment that the shortage of oil is permanent and real. As soon as most people come around to this realization, the global transportation system will begin to transition away from oil. That transition will end the oil state as it exists today.

Many OPEC members are currently engaged in huge infrastructure projects and are attempting to diversify their economies. The longer they have to develop these projects, the better chance they have of not becoming impoverished when the oil demand dries up.

So, don't expect to hear anything from them about limited supply any time soon.

Speculators and the Oil Markets

Previously, I discussed futures contracts in the context of agriculture (wheat and corn). But, they are generic instruments that can work with any commodity. In the case of oil, people speculate on the future supply and the future demand.

We all know the litany of variables in supply: war, strikes, unrest, natural disasters, success in exploration, decline in existing fields, technological advancement, etc.

Likewise, there are demand variables: chiefly the world's economic growth.

At the moment, Southwest Airlines is making money where others aren't, because they used futures to buy all of their jet fuel years in advance. They recognized fuel prices as a large variable in their profitability that they could not control. Further, they may also have suspected coming increases. At any rate, they made a very sound decision to take that risk out of their business, and they are now being handsomely rewarded for it.

Speculators are currently predicting that oil will continue to stay about where it is for the foreseeable future. I will make two points.

First, if there turns out to be more oil available at the beginning of next year than the futures prices today imply, a speculator who bought a contract to receive that crude will have to get rid of it, and the more of it there is, the lower the price that a desperate speculator will have to accept. (It is another form of speculation to not buy a futures contract, but to wait until they come due to look for deals. In speculation, there are always two participants and one of them is wrong.)

Secondly, this prediction should not surprise us. On the one hand we have billions of new people coming into the middle class. They want air conditioning, cars, electric shavers, televisions, light bulbs, computers, etc., etc., etc. That means higher energy demand. And, on the other hand, we have supply growth that is not keeping up.

It may still prove to be wrong, but at this moment it appears we aren't "out of oil" (a lot is still coming out of the ground), but effectively, we are out of oil (there isn't enough). And, that is no fault of speculators.

We all know the litany of variables in supply: war, strikes, unrest, natural disasters, success in exploration, decline in existing fields, technological advancement, etc.

Likewise, there are demand variables: chiefly the world's economic growth.

At the moment, Southwest Airlines is making money where others aren't, because they used futures to buy all of their jet fuel years in advance. They recognized fuel prices as a large variable in their profitability that they could not control. Further, they may also have suspected coming increases. At any rate, they made a very sound decision to take that risk out of their business, and they are now being handsomely rewarded for it.

Speculators are currently predicting that oil will continue to stay about where it is for the foreseeable future. I will make two points.

First, if there turns out to be more oil available at the beginning of next year than the futures prices today imply, a speculator who bought a contract to receive that crude will have to get rid of it, and the more of it there is, the lower the price that a desperate speculator will have to accept. (It is another form of speculation to not buy a futures contract, but to wait until they come due to look for deals. In speculation, there are always two participants and one of them is wrong.)

Secondly, this prediction should not surprise us. On the one hand we have billions of new people coming into the middle class. They want air conditioning, cars, electric shavers, televisions, light bulbs, computers, etc., etc., etc. That means higher energy demand. And, on the other hand, we have supply growth that is not keeping up.

It may still prove to be wrong, but at this moment it appears we aren't "out of oil" (a lot is still coming out of the ground), but effectively, we are out of oil (there isn't enough). And, that is no fault of speculators.

What Speculators Do

In the commodities markets, producers sell their product months (even years) in advance (through "futures contracts"). This helps producers plan, because they know they will receive a certain price for their efforts. Suppose that you are a farmer, and you have the choice of growing wheat or corn. Which should you plant? How do you know what the price of either will be when the harvest comes? Maybe there will be a bumper crop of one, and a near famine in the other. But which? And, how much should you spend on fertilizer? Or is the farm land even worth keeping as farm land, given the return you might or might not get? All of these questions can be quickly answered if you look up the price of the corn and wheat futures. If the going rate for corn at harvest next year is high, and wheat is low, not only do you choose the right crop, but you can answer the other questions as well.

So, who is buying these things? Again, suppose you are a company that makes corn flakes. You need wheat to do it. And, you've been burned in the past when you thought you would be able to make money, but couldn't because the wheat crop failed and you had to pay way more than you expected and lost money on every box of cereal you sold. On the other hand, some years you got lucky, and got a really good deal on wheat, but all things considered, you'd really just like predictability and a nice steady profit. Why not buy wheat years in advance for known prices? Then you can plan around it, and not have to worry about the unexpected.

But, suppose you weren't a factory owner, but a wizard weather predictor. Your models are telling you that a big drought is coming, and that the corn crop is going to be terrible. You might make some money if you bought some corn futures before anyone else realized the doom on the horizon. Then, when everyone realized there wasn't going to be enough corn, and the price went went way up, you could sell the corn you bought cheaply for a nice, fat profit. You would be speculating on the future of wheat.

There is a danger, though, that truckloads of corn are going to show up at your doorstep one Saturday, and that would not be good. So, you've got to make sure and sell the futures contract you bought (hopefully at a profit) before the contract is due.

And, here is the key: at the end, right before the contract comes due, the contracts all have to find a home for receiving the product. Then, it is a simple matter of supply and demand, and the fact that the futures contract went up and down for months on the market is irrelevant. If there is a lot of corn, the price will go down, and if there is not, the price will go up. But, this is only reflecting real world supply and demand, and not crazy speculation (as might have been the case months before the contract was due, and it wasn't clear just how much corn would be around).

So, to quickly sum up, the point of the futures markets is to bring everyone's predictions of the future together for planning purposes. The speculators help allocate resources in the future. Think about it: if the futures price for wheat is high, farmers will plant more wheat, which will cause the futures prices for wheat to fall. In that case, the futures market predicted a shortage of wheat that was avoided because of their prediction.

So, who is buying these things? Again, suppose you are a company that makes corn flakes. You need wheat to do it. And, you've been burned in the past when you thought you would be able to make money, but couldn't because the wheat crop failed and you had to pay way more than you expected and lost money on every box of cereal you sold. On the other hand, some years you got lucky, and got a really good deal on wheat, but all things considered, you'd really just like predictability and a nice steady profit. Why not buy wheat years in advance for known prices? Then you can plan around it, and not have to worry about the unexpected.

But, suppose you weren't a factory owner, but a wizard weather predictor. Your models are telling you that a big drought is coming, and that the corn crop is going to be terrible. You might make some money if you bought some corn futures before anyone else realized the doom on the horizon. Then, when everyone realized there wasn't going to be enough corn, and the price went went way up, you could sell the corn you bought cheaply for a nice, fat profit. You would be speculating on the future of wheat.

There is a danger, though, that truckloads of corn are going to show up at your doorstep one Saturday, and that would not be good. So, you've got to make sure and sell the futures contract you bought (hopefully at a profit) before the contract is due.

And, here is the key: at the end, right before the contract comes due, the contracts all have to find a home for receiving the product. Then, it is a simple matter of supply and demand, and the fact that the futures contract went up and down for months on the market is irrelevant. If there is a lot of corn, the price will go down, and if there is not, the price will go up. But, this is only reflecting real world supply and demand, and not crazy speculation (as might have been the case months before the contract was due, and it wasn't clear just how much corn would be around).

So, to quickly sum up, the point of the futures markets is to bring everyone's predictions of the future together for planning purposes. The speculators help allocate resources in the future. Think about it: if the futures price for wheat is high, farmers will plant more wheat, which will cause the futures prices for wheat to fall. In that case, the futures market predicted a shortage of wheat that was avoided because of their prediction.

Energy Independence

Many politicians are now talking about the importance of drilling in the United States for oil so that America can become "energy independent". This argument is, rhetorically, the anti-global-warming argument. It goes something like this:

1) The price of oil is too high! We need to drill!

2) You can't drill more oil, we have to deal with global warming. Go solar!

3) We should develop new energy, but we can't be held hostage to dangerous regimes. Energy Independence!

I was thinking about "energy independence", and realized that I had misunderstood the real meaning of that term. Suppose that the U.S. Congress lifted the ban on various parts of the country, and opened them up to drilling. Major oil companies would move in, buy leases, set up deep water drilling rigs, and start pumping crude. Then what? Then, they would sell their new barrels of oil on the *international* commodities market.

In other words, drilling in the U.S. would increase production for the world, but that new production would be shared with everyone. So, the "independence" part would really be to dilute the share of global supply provided by the bad guys.

I think most people, when they hear the phrase, think that the U.S. would get every barrel of oil drilled in the U.S. And, that might practically be the case, since local oil should be the cheapest for U.S. consumers if only because of transport costs. But, unless we nationalize the oil industry, oil pumped in the U.S. isn't "American Oil" until America buys it.

(I'm certainly NOT advocating nationalizing the oil industry.)

1) The price of oil is too high! We need to drill!

2) You can't drill more oil, we have to deal with global warming. Go solar!

3) We should develop new energy, but we can't be held hostage to dangerous regimes. Energy Independence!

I was thinking about "energy independence", and realized that I had misunderstood the real meaning of that term. Suppose that the U.S. Congress lifted the ban on various parts of the country, and opened them up to drilling. Major oil companies would move in, buy leases, set up deep water drilling rigs, and start pumping crude. Then what? Then, they would sell their new barrels of oil on the *international* commodities market.

In other words, drilling in the U.S. would increase production for the world, but that new production would be shared with everyone. So, the "independence" part would really be to dilute the share of global supply provided by the bad guys.

I think most people, when they hear the phrase, think that the U.S. would get every barrel of oil drilled in the U.S. And, that might practically be the case, since local oil should be the cheapest for U.S. consumers if only because of transport costs. But, unless we nationalize the oil industry, oil pumped in the U.S. isn't "American Oil" until America buys it.

(I'm certainly NOT advocating nationalizing the oil industry.)

Wednesday, June 11, 2008

Why Oil Costs So Much

Perhaps you have seen the circus in the U.S. Congress recently, where they have proposed "windfall" profit taxes on the five largest oil companies. And, where one Senator pleaded with a CEO in a strained voice, asking "Don't you see what you're doing to your country?"

Or, in another fit of irrationality, Congress' newly proposed legislation to undo the Carter reform of pricing oil in a commodities market. They have proposed this to thwart the greedy Wall Street speculators.

Surely, there must be evil lurking somewhere. There must be some scapegoat to pay the price.

But, it isn't to be. I did a little research on my own a few days ago, and convinced myself of what BP has provided in its own Statistical Review of Global Energy 2008.

In their report, they point out that oil production FELL by .2% in 2007, despite through the roof prices. In fact, I found on Wikipedia that oil production has been roughly flat since the beginning of 2005.

What does this mean? Normally, when demand falls, the price drops, and then the supply falls. The reason that supply falls is that each oil well has a price per barrel where it makes economic sense to remove it from the ground. In other words, if it took $100 per barrel to pump the stuff out of the ground, why do it if the price is only $90 per barrel on the open market? You'd be losing $10 per barrel that you sold, and you wouldn't last long in the oil business.

Up to 2005, this relationship is solidly in place. You can put the price chart next to the supply chart, and see them moving together. But starting in 2005, the production stops going up; it's as if it hits a limit. The price keeps rising, because the world economy is growing, and it needs more oil to function. Those prices should have caused more expensive barrels in the ground to be pumped up - but they haven't.

Why? My thinking at the moment is that high prices are stimulating exploration and production - the problem is that old production is falling away, as old fields decline. It may be that technology will bail us out of this (new ways of pumping previously unreachable oil), or that new production projects that can meet the world's demand have long lead times. But, at 3.5 years of elevated prices (and counting), my hope there is starting to run thin.

Basically, this is supply and demand. Not greedy speculators and not evil oil companies. This is the result of billions of people around the world emerging from poverty and improving their material life style.

Or, in another fit of irrationality, Congress' newly proposed legislation to undo the Carter reform of pricing oil in a commodities market. They have proposed this to thwart the greedy Wall Street speculators.

Surely, there must be evil lurking somewhere. There must be some scapegoat to pay the price.

But, it isn't to be. I did a little research on my own a few days ago, and convinced myself of what BP has provided in its own Statistical Review of Global Energy 2008.

In their report, they point out that oil production FELL by .2% in 2007, despite through the roof prices. In fact, I found on Wikipedia that oil production has been roughly flat since the beginning of 2005.

What does this mean? Normally, when demand falls, the price drops, and then the supply falls. The reason that supply falls is that each oil well has a price per barrel where it makes economic sense to remove it from the ground. In other words, if it took $100 per barrel to pump the stuff out of the ground, why do it if the price is only $90 per barrel on the open market? You'd be losing $10 per barrel that you sold, and you wouldn't last long in the oil business.

Up to 2005, this relationship is solidly in place. You can put the price chart next to the supply chart, and see them moving together. But starting in 2005, the production stops going up; it's as if it hits a limit. The price keeps rising, because the world economy is growing, and it needs more oil to function. Those prices should have caused more expensive barrels in the ground to be pumped up - but they haven't.

Why? My thinking at the moment is that high prices are stimulating exploration and production - the problem is that old production is falling away, as old fields decline. It may be that technology will bail us out of this (new ways of pumping previously unreachable oil), or that new production projects that can meet the world's demand have long lead times. But, at 3.5 years of elevated prices (and counting), my hope there is starting to run thin.

Basically, this is supply and demand. Not greedy speculators and not evil oil companies. This is the result of billions of people around the world emerging from poverty and improving their material life style.

Tuesday, February 5, 2008

Subscribe to:

Posts (Atom)